Industry Statistics and Rankings

How does this industry perform in Poland compared to Europe?

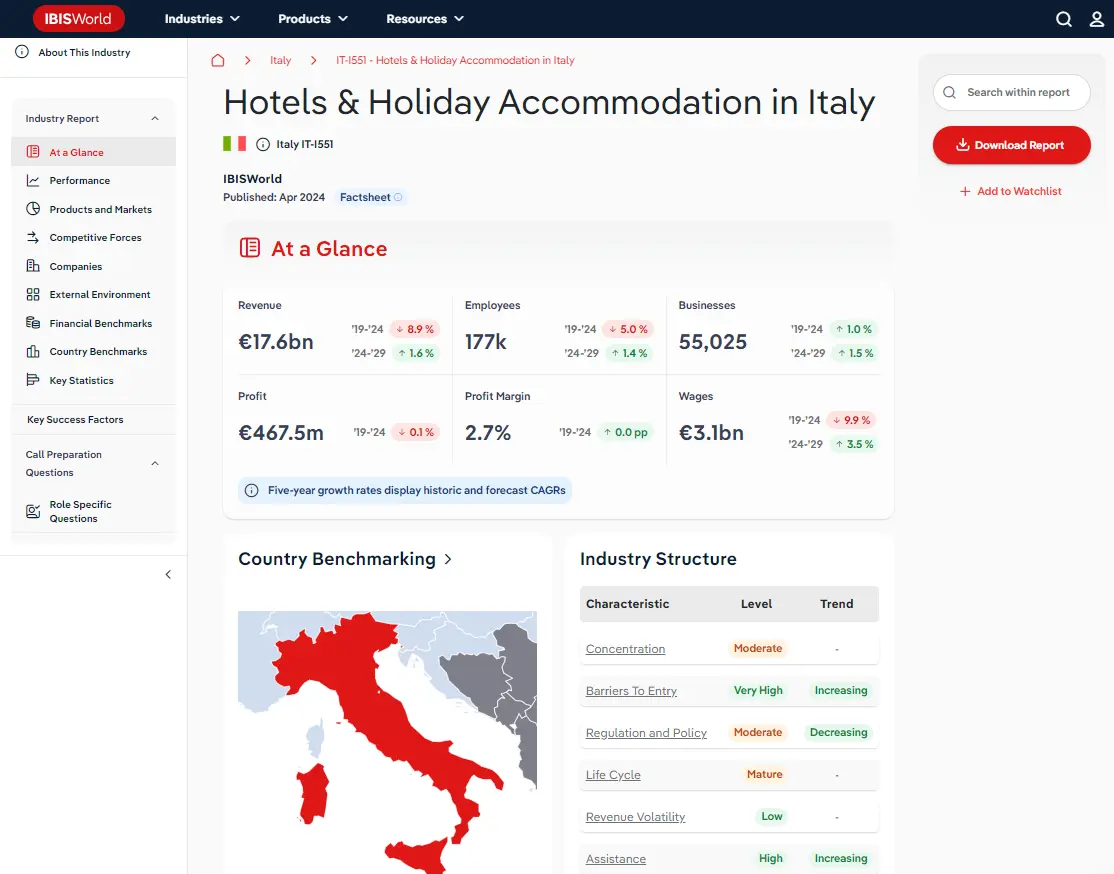

Country Benchmarking

Industry Data Poland

Ranking are out of 37 European countries for which IBISWorld provides country-level factsheets.

Revenue

#9 In EuropeBusiness

#10 In EuropeEmployees

#9 In EuropeWages

#10 In EuropeOver the five years through 2025, industry revenue is expected to drop at a compound annual rate of 5.8%. Specialist food retailers in the UK have endured a turbulent period marked by soaring costs, fragile consumer confidence, and intensifying competition. Supermarkets and discounters intensified pressure, expanding private label ranges into premium and organic lines. In response, specialists leaned on differentiation through provenance, artisanal quality, sustainability, and closer community ties, with many embracing digital tools, home delivery, and loyalty initiatives. Evolving consumer habits also spurred adoption of grocery-plus models, blending retail and food service to deliver ready-to-eat, health-focused, and locally sourced meals—an increasingly important lever of resilience and growth.Operating expenses rose sharply due to surging ingredient, feed, energy, and labour costs, squeezing margins even as food inflation eased from an EU peak of 19.3% in 2023 to 3.1% by mid-2025. Stubborn input costs and stagnant household budgets kept value top of mind for consumers, with over a third of UK shoppers still cutting back on groceries. Labour costs climbed with minimum wage hikes and tight labour markets, challenging a sector reliant on personal service and skilled staff. Independents often turned to flexible or family labour, while larger chains absorbed premium wage pressures. Energy shocks in 2022 pushed many small shops to the brink, with government relief proving vital. In 2025, revenue is expected to dip by 4.7% to €99.5 billion, while profit is anticipated to absorb 8.7% of revenue. Over the five years through 2030, revenue is expected to dip at a compound annual growth rate of 1.5% reaching €92.2 billion, while profit is anticipated to remain under pressure from intense competition reaching 7.2% of revenue. Specialist food retailers face a complex future shaped by labour pressures, intensifying competition, and shifting consumer values. Persistent labour shortages and rising wages will remain a defining challenge, with larger chains turning to automation to offset costs, while smaller shops balance authenticity with cautious digital adoption, wary of undermining their artisanal identity. Competitive pressure will sharpen as supermarkets expand premium private labels and capture more foot traffic through scale and strategic locations. To stand out, specialist retailers must lean into differentiation, offering experiences such as tastings, workshops and masterclasses, alongside stronger storytelling and digital engagement. Consumer behaviour will reinforce opportunities for specialists. Health, sustainability and premiumisation are driving demand for fresh, ethically sourced and high-quality food. Younger shoppers, in particular, expect traceability and are willing to pay premiums for welfare-friendly, clean-label products.

Enterprises

Number of businesses in 2025

Biggest companies in the Food Retailing in Poland

| Company | Market Share (%)

2025 | Revenue (€m)

2025 | Profit (€m)

2025 | Profit Margin (%)

2025 |

|---|---|---|---|---|

Boulangeries Paul SAS | 897.7 | 111.5 | 12.4 |

Access statistics and analysis on all 1 companies with purchase. View purchase options.

Top Questions Answered in this Report

Unlock comprehensive answers and precise data upon purchase. View purchase options.

What is the market size of the Food Retailing industry in Poland in 2025?

The market size of the Food Retailing industry in Poland is €6.0bn in 2025.

How many businesses are there in the Food Retailing industry in Poland in 2025?

There are 10,179 businesses in the Food Retailing industry in Poland, which has declined at a CAGR of 3.1 % between 2020 and 2025.

Has the Food Retailing industry in Poland grown or declined over the past 5 years?

The market size of the Food Retailing industry in Poland has been growing at a CAGR of 0.5 % between 2020 and 2025.

What is the forecast growth of the Food Retailing industry in Poland over the next 5 years?

Over the next five years, the Food Retailing industry in Poland is expected to grow.

What are the biggest companies in the Food Retailing industry in Poland?

The biggest company operating in the Food Retailing industry in Poland is Boulangeries Paul SAS

What does the Food Retailing industry in Poland include?

Meat and Fruit and vegetables are part of the Food Retailing industry in Poland.

Which companies have the highest market share in the Food Retailing industry in Poland?

The company holding the most market share in the Food Retailing industry in Poland is Boulangeries Paul SAS.

How competitive is the Food Retailing industry in Poland?

The level of competition is moderate and steady in the Food Retailing industry in Poland.

Related Industries

This industry is covered in 37 countries

Domestic industries

Competitors

Complementors

International industries

Table of Contents

About this industry

Industry definition

This industry consists of food retailers, which may sell fruit, vegetable, meat, fish and bakery products. This industry excludes the retail sale of food by mass retailers such as supermarkets and department stores.

Related Terms

CRUSTACEANSCULTIVATED MEAT ORGANIC FOOD CONFECTIONERYWhat's included in this industry?

MeatFruit and vegetables Seafood SeafoodCompanies

Boulangeries Paul SASIndustry Code

4721 - Retail sale of food in specialized stores in Poland

View up to 1 companies with purchase. View purchase options.

Performance

Revenue Highlights

Trends

- Revenue

- 2025 Revenue Growth

- Revenue Volatility

Employment Highlights

Trends

- Employees

- Employees per Business

- Revenue per Employee

Business Highlights

Trends

- Businesses

- Employees per Business

- Revenue per Business

Profit Highlights

Trends

- Total Profit

- Profit Margin

- Profit per Business

Current Performance

Charts

- Revenue

- Employees

- Business

- Profit

Analysis

What's driving current industry performance in the Food Retailing in Poland industry?

Outlook

Analysis

What's driving the Food Retailing in Poland industry outlook?

Volatility

Analysis

What influences volatility in the Food Retailing in Poland industry?

Charts

- Industry Volatility vs. Revenue Growth Matrix

Life Cycle

Analysis

What determines the industry life cycle stage in the Food Retailing in Poland industry?

Charts

- Industry Life Cycle Matrix

Products and Markets

Highlights

Trends

- Largest Market

- Product Innovation

Key Takeaways

Income and preferences dictate specialised food markets. High-income households seek premium food products, while lower-income consumers prioritise affordability, meaning they tend to opt for supermarket food offerings.

Products and Services

Charts

- Products and Services Segmentation

Analysis

How are the Food Retailing in Poland industry's products and services performing?

Analysis

What are innovations in the Food Retailing in Poland industry's products and services?

Major Markets

Charts

- Major Market Segmentation

Analysis

What influences demand in the Food Retailing in Poland industry?

International Trade

Highlights

- Total Imports into Poland

- Total Exports into Poland

Heat maps

- Industry Concentration of Imports by Country

- Industry Concentration of Exports by Country

Data Tables

Value and annual change (%) included

- Number of Imports and Exports by European Country (2025)

Competitive Forces

Highlights

Trends

- Concentration

- Competition

- Barriers to Entry

- Substitutes

- Buyer Power

- Supplier Power

Key Takeaways

High fragmentation in the industry prevents concentration. industry’s high fragmentation limits concentration, as food retailers are typically popular within their local area, with the majority of food retailers being independent.

Supply Chain

Charts

Buyer and supply industries

Geographic Breakdown

Business Locations

Heat maps

- Share of Total Industry Establishments by Region (2025)

Data Tables

- Number of Establishments by Region (2025)

Charts

- Share of Establishments vs. Population of Each Region

Analysis

What regions are businesses in the Food Retailing in Poland located?

Companies

Data Tables

Top 1 companies by market share:

- Market share (2025)

- Revenue (2025)

- Profit (2025)

- Profit margin (2025)

External Environment

Highlights

Trends

- Regulation & Policy

- Assistance

Key Takeaways

The Food Safety Act 1990 plays a big role in the industry. The act stipulates that all businesses involved in food must ensure that they do not include anything in the food that is damaging to the health of those eating it.

External Drivers

Analysis

What demographic and macroeconomic factors impact the Food Retailing in Poland industry?

Financial Benchmarks

Highlights

Trends

- Profit Margin

- Average Wage

- Largest Cost

Key Takeaways

Premium food retailers earn a larger profit. Food retailers selling premium groceries can retail at higher prices and earn a higher profit.

Cost Structure

Charts

- Share of Economy vs. Investment Matrix

-

Industry Cost Structure Benchmarks:

- Marketing

- Depreciation

- Profit

- Purchases

- Wages

- Rent

- Utilities

- Other

Analysis

What trends impact cost in the Food Retailing in Poland industry?

Key Ratios

Data tables

- IVA/Revenue (2015-2030)

- Imports/Demand (2015-2030)

- Exports/Revenue (2015-2030)

- Revenue per Employee (2015-2030)

- Wages/Revenue (2015-2030)

- Employees per Establishment (2015-2030)

- Average Wage (2015-2030)

Country Benchmarks

European Leaders & Laggards

Data Tables

Top and bottom five countries listed for each:

- Revenue Growth (2025)

- Business Growth (2025)

- Job Growth (2025)

European Country Performance

Data Tables

Rankings available for 37 countries. Statistics ranked include:

- IVA/Revenue (2025)

- Imports/Demand (2025)

- Exports/Revenue (2025)

- Revenue per Employee (2025)

- Wages/Revenue (2025)

- Employees per Establishment (2025)

- Average Wage (2025)

Structural Comparison

Data Tables

Trends in 37 countries benchmarked against trends in Europe

- Concentration

- Competition

- Barriers to Entry

- Buyer Power

- Supplier Power

- Volatility

- Capital Intensity

- Innovation

- Life Cycle

Key Statistics

Industry Data

Data Tables

Including values and annual change:

- Revenue (2015-2030)

- IVA (2015-2030)

- Establishments (2015-2030)

- Enterprises (2015-2030)

- Employment (2015-2030)

- Exports (2015-2030)

- Imports (2015-2030)

- Wages (2015-2030)

Methodology

Where does IBISWorld source its data?

IBISWorld is a world-leading provider of business information, with reports on 5,000+ industries in Australia, New Zealand, North America, Europe and China. Our expert industry analysts start with official, verified and publicly available sources of data to build an accurate picture of each industry.

Each industry report incorporates data and research from government databases, industry-specific sources, industry contacts, and IBISWorld's proprietary database of statistics and analysis to provide balanced, independent and accurate insights.

IBISWorld prides itself on being a trusted, independent source of data, with over 50 years of experience building and maintaining rich datasets and forecasting tools.

To learn more about specific data sources used by IBISWorld's analysts globally, including how industry data forecasts are produced, visit our Help Center.

France

France

Italy

Italy

Spain

Spain